Blinkit in 2026: Revenue, Market Share, Profitability, and What Comes Next

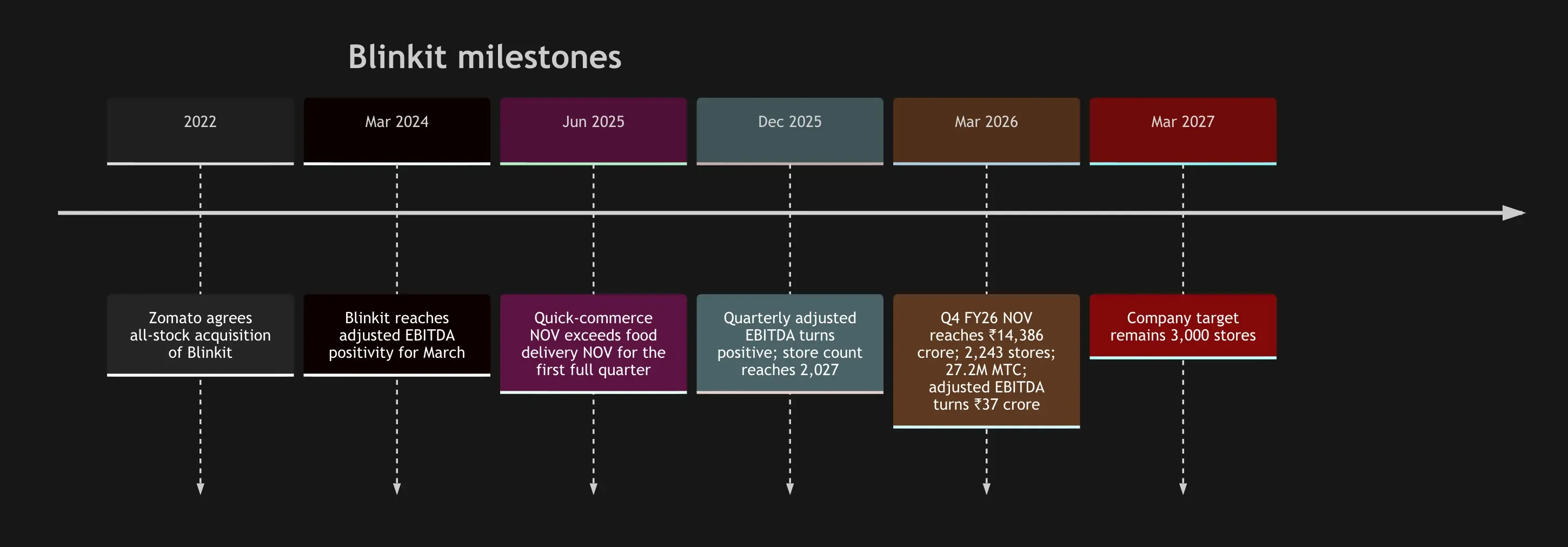

Blinkit is no longer just Eternal’s quick-commerce side business. It is now the company’s clearest growth engine and the strongest public benchmark for how scaled quick commerce in India can look when growth and operating discipline start showing up together. In Q1 FY26, Blinkit’s quick-commerce NOV exceeded Zomato food delivery NOV for the first full quarter. By Q4 FY26, Blinkit had reached ₹14,386 crore in NOV, 2,243 dark stores, and ₹37 crore in adjusted EBITDA. Public reporting around the March-quarter results also put Blinkit at 27.2 million monthly transacting users, about 274 million quarterly orders, and net AOV around ₹525.

That said, if you read Blinkit only through reported revenue, you will misread the business. Eternal began transitioning Blinkit from a marketplace model to inventory ownership in Q1 FY26, and said quick-commerce revenue would start looking much closer to NOV as that shift progressed. By Q3 FY26, about 90% of Blinkit NOV was already on own inventory; Eternal also said more than half of the expected one percentage point margin accretion from that change had already been captured. So yes, Blinkit’s FY26 revenue from operations reached ₹37,779 crore and Q4 revenue reached ₹13,232 crore, but those numbers are not clean like-for-like comparisons with earlier commission-style reporting. For a serious update, NOV is the metric to lead with.

Stay Updated on QA & Tech Trends

Get insights on testing strategies, mobile QA, and industry updates. Join 2,000+ professionals.

Read the revenue correctly

Eternal has explicitly told investors that Blinkit’s headline revenue began to inflate mechanically once the platform moved toward owning inventory rather than only taking marketplace commissions. In the same Q3 FY26 letter, Eternal explained that like-for-like consolidated adjusted-revenue growth was materially lower than raw growth because reported quick-commerce revenue now includes the full value of goods sold rather than just commission income. That is why a 600%-plus jump in Blinkit revenue should not be interpreted as equivalent to a 600%-plus jump in consumer demand. Demand grew very fast; accounting grew even faster.

Blinkit by the numbers in FY26

Blinkit entered FY26 with a huge scale jump already underway. In Q1 FY26, Blinkit added 243 net new stores to reach 1,544 stores, while monthly transacting customers grew from 7.6 million to 16.9 million year over year. Media coverage around that quarter reported Blinkit’s GOV at ₹11,821 crore and NOV at roughly ₹9,230 crore, marking the first quarter in which Blinkit’s quick-commerce order value overtook Eternal’s food-delivery business for the full period.

By Q3 FY26, Blinkit had reached 2,027 stores and reported quarterly adjusted EBITDA breakeven for the first time, at ₹4 crore. Eternal credited that improvement to supply-chain cost efficiencies, a favorable shift toward long-tail categories, operating leverage, and margin benefits from the ongoing move to own inventory. Management also kept its long-term confidence intact, saying mature geographies already show the shape of the end-state model: Delhi NCR as a whole was running at roughly 3.5% adjusted EBITDA margin, while Gurgaon and Noida were around 5%.

In Q4 FY26, Blinkit kept growing and widened the operating gap over rivals. Eternal said Blinkit’s NOV rose 95.4% year over year to ₹14,386 crore, with 216 net new stores taking the network to 2,243. Blinkit’s adjusted EBITDA rose to ₹37 crore. Public reporting on the quarter also showed monthly transacting users at 27.2 million, net AOV at ₹525, and quarterly orders at roughly 274 million. Blinkit’s FY26 revenue from operations reached ₹37,779 crore.

The milestones below capture the operating transition from acquisition-era turnaround story to scaled, increasingly profitable quick-commerce leader. The acquisition milestone comes from Reuters reporting on the 2022 all-stock deal, while the later milestones come from Eternal’s official shareholder letters and Q4 FY26 earnings materials.

Why Blinkit is pulling ahead

Blinkit’s advantage is no longer just “it grew early.” Eternal’s own commentary points to something more durable. Management says the business improved margins through supply-chain cost efficiencies, long-tail category mix, and operating leverage—not through a last-minute cost-cutting push. That matters because it suggests Blinkit’s profitability is coming from system design, assortment depth, and density, not from slowing down expansion.

The own-inventory shift is a major part of this story. Eternal said in Q1 FY26 that controlling inventory should give Blinkit more leverage on margins and help it push harder on assortment. By Q3 FY26, 90% of Blinkit NOV was already being fulfilled on own inventory, and the company said more than half of the expected margin accretion from that model shift had already been captured. In plain English: Blinkit is acting more like a tightly controlled retail-and-logistics system and less like a pure marketplace.

The company also thinks mature-city economics travel. Eternal said smaller cities look promising because the net AOV gap between large and small cities was only around 10%, while operating costs in smaller cities are lower. At the same time, management made clear that exact metro-versus-non-metro splits are intentionally not disclosed. So the right update is not to invent a geographic mix, but to say that Blinkit is clearly diversifying beyond metros while keeping its exact metro/tier-2 store split unspecified. That is consistent with later Q4 commentary, where management said the dark-store mix is changing over time as more growth comes from geographic diversification. Blinkit’s own public careers page also lists service in a long roster of non-metro cities, from Agra and Bareilly to Guntur, Rajkot, Siliguri, and Warangal, which supports the broader point without pretending to know the exact store split.

One more nuance matters. Blinkit is expanding into more categories, but it still does not publish a grocery-versus-non-grocery revenue split in the latest official materials. Management has said assortment expansion and non-grocery penetration are key growth drivers, but did not disclose the category mix. The same is true for advertising and private labels. Blinkit clearly has a real retail-media business—Brand Central is its self-serve ad platform, and management says quick commerce already generates more ad income as a percentage of NOV than food delivery—but Eternal still does not publish Blinkit’s absolute FY26 ad revenue or private-label revenue.

Blinkit vs Zepto

The sharpest comparison now is Blinkit versus Zepto. Zepto has closed some of the scale gap, especially on order velocity in dense markets, and its IPO filing has made it a much more transparent company than most private rivals. But Blinkit still leads on the combination that matters most: larger order-value scale, broader network maturity, and operating profitability. Reuters reported Zepto’s FY26 revenue at ₹22,623.58 crore, but also FY26 losses of ₹5,905.19 crore. ET and Mint reported Q4 FY26 revenue of ₹7,498 crore, Q4 net loss of about ₹1,538–1,539 crore, and more than 550,000 daily orders in May 2026. Zepto’s own public-market paperwork, as reported by Moneycontrol and Mint, also pointed to 1,139 dark stores across 66 cities, 210 million Q4 orders, ₹24,816 crore in FY26 NRV, and ₹1,636 crore in FY26 ad revenue.

Blinkit, by contrast, is still the leader on scale and operating discipline. Reuters’ latest public market-share snapshot available through Datum put Blinkit at 48% share at the start of 2026. ET later reported Blinkit at around 650,000 daily orders in May 2026, ahead of Zepto’s 550,000. Eternal’s own materials showed a profitable Q4 FY26 on adjusted EBITDA, 2,243 stores, and ongoing confidence in a long-term 5%–6% margin model.

Metric | Blinkit | Zepto |

Latest publicly cited market-share snapshot | 48% of India quick commerce in Reuters/Datum’s Jan. 2026 snapshot

| Unspecified in primary latest public filing coverage reviewed |

Latest quarterly demand metric | Q4 FY26 NOV: ₹14,386 crore

| Q4 FY26 NRV: ₹8,134 crore

|

FY26 revenue | ₹37,779 crore

| ₹22,623.58 crore

|

Latest quarterly profitability status | Adjusted EBITDA +₹37 crore in Q4 FY26

| Net loss ₹1,538–1,539 crore in Q4 FY26; not yet profitable

|

Order counts | Around 650,000 daily orders in May 2026; about 274 million Q4 orders reported in public coverage

| More than 550,000 daily orders in May 2026; 210 million Q4 orders

|

Dark-store network | 2,243 stores; exact city count publicly unspecified in latest official materials

| 1,139 dark stores across 66 cities

|

Ad monetisation | Blinkit ad revenue exists but FY26 absolute amount is unspecified publicly; management says QC ad revenue as % of NOV is already higher than food delivery

| FY26 ad revenue ₹1,636 crore, around 7.8% of NRV

|

The simple takeaway is that Zepto now looks credible as the number-two challenger on order momentum, but Blinkit remains the company that has translated quick-commerce scale into visible operating profit. That is the real reason the 2026 version of this story is stronger than the old “Blinkit surpasses Zomato” angle.

The broader competitive field

Blinkit is still the benchmark, but the field behind it is now large enough that any serious rewrite needs a comparison table rather than a generic “competition exists” paragraph.

Company | Latest disclosed scale snapshot | Profitability snapshot | Network snapshot | What matters now |

Blinkit | Q4 FY26 NOV ₹14,386 crore; around 27.2M MTC; public reporting puts Q4 orders near 274M

| Adjusted EBITDA +₹37 crore in Q4 FY26

| 2,243 stores; mix shifting toward more geographic diversification, exact metro/tier-2 split unspecified

| Still the scale and profitability leader |

Swiggy Instamart | Q4 FY26 GOV ₹7,881 crore, NOV ₹5,675 crore, 112.6M orders, 13.3M MTUs, AOV ₹700

| Adjusted EBITDA -₹858 crore; contribution margin -1.8% of GOV in Q4 FY26

| 1,143 stores across 129 cities

| Big network, but still materially behind Blinkit on profitability and order scale |

Zepto | FY26 revenue ₹22,623.58 crore; FY26 NRV ₹24,816 crore; 210M Q4 orders; 550K+ daily orders in May 2026

| Q4 FY26 net loss about ₹1,538–1,539 crore; FY26 net loss ₹5,905.19 crore

| 1,139 dark stores across 66 cities

| Most credible private challenger, still not close on profit |

Flipkart Minutes | Exact revenue, orders, and market share unspecified publicly; ET and Moneycontrol reported roughly 750–800 stores in March–April 2026 and an internal push to add 800 more in 2026

| Unspecified publicly | Roughly 750–800 stores in early 2026, with aggressive expansion under way

| A serious infrastructure build, especially relevant for pressure in tier-2 markets |

Amazon Now | Exact revenue and orders unspecified publicly; official Amazon India communication said the service is scaling to 100 cities with 1,000+ micro-fulfilment centres

| Unspecified publicly | Official plan: 100 cities, 1,000+ micro-fulfilment centres; April 2026 public reporting said it was then operating in Delhi-NCR, Mumbai, and Bengaluru

| Deep capital, long time horizon, and the broadest cross-category retail muscle |

JioMart hyper-local | Q3 FY26 official presentation said 1.6M daily orders run-rate; Q4 official release said average daily orders were up 29% QoQ and 300%+ YoY | Quick-commerce profitability unspecified in the latest official Q4 release reviewed | 5,100+ pin codes, 1,200+ cities, and 3,100+ stores; non-grocery quick hyper-local network expanded to 682 electronics and 1,700+ fashion & lifestyle stores with 2-hour delivery promise

| Not a pure dark-store clone of Blinkit; it leverages Reliance’s wider store network, which makes it potentially dangerous over time |

This table is why the old blog’s framing needs to change. The real story is no longer “can Blinkit beat Zomato food delivery?” It already changed Eternal’s business mix. The bigger question now is whether Blinkit can stay ahead when every other serious retail and delivery platform is building speed, density, or both.

Risks that still matter

Blinkit looks stronger than it did a year ago, but it is not risk-free. The first risk is regulatory. Reuters reported in January 2026 that India’s government ordered Blinkit, Zepto, and Swiggy to stop promoting grocery delivery as a “10-minute” service after concerns around rider safety and pay practices. That is not just a tagline issue. It goes directly to the core consumer promise around speed and how the category is marketed.

The second risk is antitrust and channel conflict. Reuters reported that India’s biggest group of retail distributors had asked the competition regulator to investigate Blinkit, Swiggy, and Zepto for alleged predatory pricing. Whether or not that goes anywhere legally, it underlines a broader truth: quick commerce has become big enough to trigger organized resistance from offline trade and distribution networks.

The third risk is execution and compliance. Blinkit’s growth depends on dark-store hygiene, food handling, rider economics, and local compliance all holding together at scale. ET reported last year that Maharashtra’s FDA suspended the food licence of a Blinkit dark store in Pune over non-compliance. One store is not a business thesis, but in a network business with thousands of locations, compliance incidents can multiply if process discipline slips.

The fourth risk is simpler and more financial: competition can still hit margins. Eternal itself has said Blinkit’s profitability is not guaranteed quarter to quarter and that irrational competition can distort demand toward discounted, lower-margin categories. Management also said that if discounting tactics from rivals start meaningfully hurting Blinkit’s business, the company would have to respond, which could affect margins. That warning belongs in the rewrite because it is straight from management, not a bearish extrapolation.

What to watch in 2027

Blinkit’s near-term direction is clear even if every exact metric is not. Eternal said in Q3 FY26 that it remained on track for 3,000 stores by March 2027, and repeated in the Q4 FY26 earnings call that it was still firmly on track for that goal. Management also said Blinkit should be thought of as a business capable of roughly 60% CAGR over the next three years, although the older expectation of 100% near-term growth no longer holds.

The most likely strategic moves over the next year are also clear from management commentary. Expect more geographic diversification beyond the top metros. Expect more assortment expansion, especially in categories that deepen wallet share rather than just add headline SKU count. Expect continued ad monetisation, because management has openly said it will take more ad income if the business can support it. Expect more selective use of automation and capex wherever Blinkit can justify it on ROCE. And expect Blinkit to stay disciplined on pricing until competition forces a different choice.

At the group level, Eternal has now said it wants to reach $20 billion in B2C NOV by FY28 and $1 billion in adjusted EBITDA by FY29. Eternal has several businesses, but Blinkit is obviously central to that ambition. That makes the 2027 outlook straightforward: Blinkit is no longer being judged on whether quick commerce can be built at scale in India. It is being judged on whether it can stay the benchmark while the rest of the market catches up.

Blinkit has moved from being the market’s fastest-growing curiosity to its most important operating test case. The business is already large. The margins have turned. The next battle is whether that lead can survive a much more crowded field.

Continue reading

More articles from the Quash editorial desk.